The 2026 Roth Catch-Up Rule

A new federal law, the SECURE 2.0 Act, changes how some people make catch-up contributions to their 401(k) beginning in 2026. If you're 50 or older and you're a higher earner, your catch-up contributions now go into the Roth side of your plan instead of the pre-tax side. Below is a plain-language walk-through of what's changing, whether it affects you, and what (if anything) you need to do.

Specific implementation may vary depending on your employer’s plan.

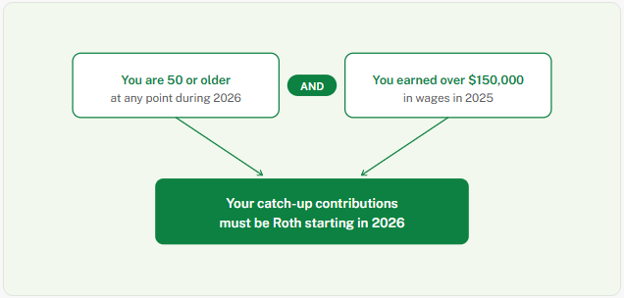

Does this affect you?

This change applies only if both of these are true for you:

If only one of these is true, or neither, nothing changes for you. You can keep contributing exactly the way you do now.

A quick refresher on catch-up contributions

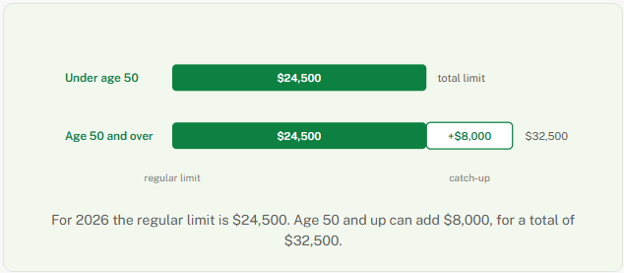

Each year the IRS sets a limit on how much you can put into your 401(k). Once you reach age 50, you're allowed to save an extra amount on top of that limit. That extra amount is your catch-up contribution.

If you're between 60 and 63 and your plan allows it, your catch-up can be larger — up to $11,250, for a total of $35,750. This is sometimes called the super catch-up.

What's changing?

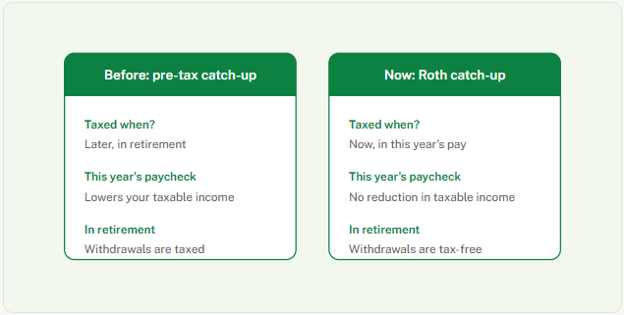

In the past, you could make catch-up contributions with pre-tax dollars, which lowered your taxable income for the year. Under the new rule, higher earners make those catch-up dollars as Roth instead. Roth money is taxed now, but qualified withdrawals in retirement are generally not subject to federal income tax. Everything else about your 401(k) stays the same. Only the catch-up portion is affected.

How it works during the year

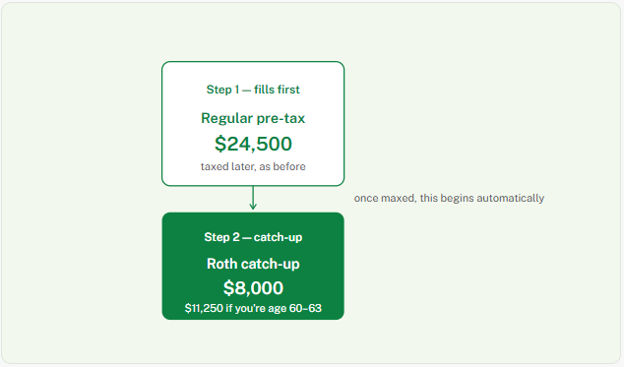

You don't have to divide your paycheck into two kinds of contributions yourself. Your regular pre-tax contributions come out first. In most plans, catch-up contributions will be treated as Roth once the regular limit is reached.

Do you need to do anything?

For most people, no. If you already contribute pre-tax and you want to keep saving toward a catch-up, in most plans, catch-up contributions will be treated as Roth once the regular limit is reached. You'd only need to submit a deferral change form if you want to stop your 401(k) contributions before the Roth portion begins.

The simple version: keep contributing the way you already do. In most plans, catch-up contributions will be treated as Roth once the regular limit is reached.

A few things worth knowing

Any Roth contributions you make earlier in the year count toward your Roth catch-up.

If your plan doesn't offer a Roth option, your ability to make catch-up contributions may be limited under current rules if a Roth option is not available.

If your income comes only from self-employment — for example, a partner or sole proprietor with no W-2 wages — this rule doesn't require your catch-up to be Roth.

The larger $11,250 super catch-up applies only to ages 60 through 63, and only if your plan allows it.

If you're not sure where you stand, your plan administrator can confirm whether this applies to you and walk you through your options. We're glad to help.

The $150,000 figure is generally based on your prior-year Social Security (FICA) wages, as reported on your W-2. The 2026 contribution figures shown here are the IRS limits and may differ from your plan's specific provisions. This guide is general information, not tax or legal advice.